We think Opera collapses on its own worsening financials

Opera: Phantom of the Turnaround – 70% Downside

Published on January 16, 2020

Opera: Phantom of the Turnaround – 70% Downside

Published on January 16, 2020

Summary (NASDAQ: OPRA)

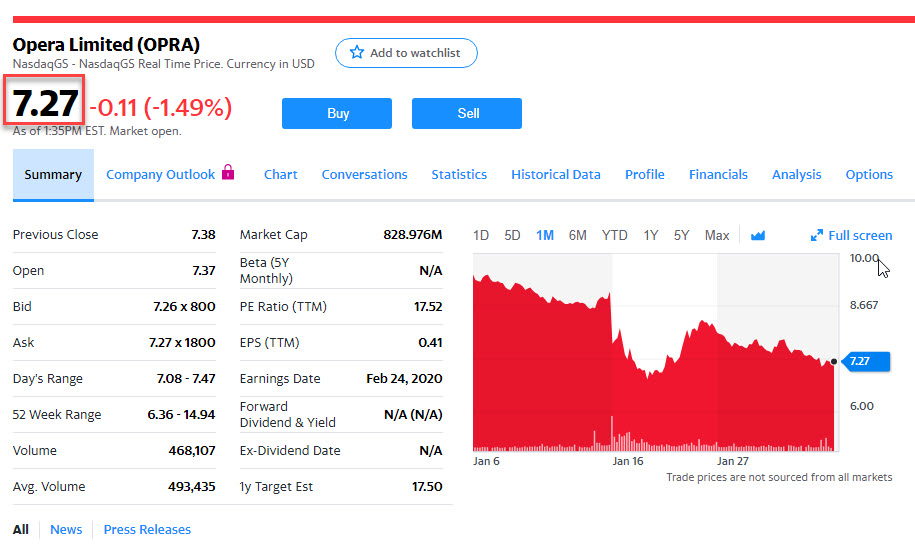

- Opera went public in mid-2018 based largely on prospects for its core browser business. Now, its browser market share is declining rapidly, down ~30% since its IPO.

- Browser gross margins have collapsed by 22.6% in just one year. Opera has swung to negative $12 million in LTM operating cash flow, compared to positive cash flow of $32 million for the comparable 2018 period.

- Opera was purchased by a China-based investor group prior to its IPO. The group’s largest investor and current Opera Chairman/CEO was recently involved in a Chinese lending business that listed in the U.S. and saw its shares plunge more than 80% in just 2 years amid allegations of fraud and illegal lending practices.

- Post IPO, Opera has now also made a similar and dramatic pivot into predatory short-term loans in Africa and India, deploying deceptive ‘bait and switch’ tactics to lure in borrowers and charging egregious interest rates ranging from ~365-876%.

- Most of Opera’s lending business is operated through apps offered on Google’s Play Store. In August, Google tightened rules to curtail predatory lending and, as a result, Opera’s apps are now in black and white violation of numerous Google rules.

- Given that the vast majority of Opera’s loans are disbursed through Android apps, we think this entire line of business is at risk of disappearing or being severely curtailed when Google notices.

- Instead of disclosing to investors that its “high-growth” microfinance segment could be imperiled by these new rules, Opera instead immediately raised $82 million in a secondary offering without disclosing Google’s changes to investors.

- Opera’s short-term loan business now accounts for over 42% of the company’s revenue and is responsible for eye-popping top line “growth”. Meanwhile, the segment experienced massive defaults (~50% of lending revenue) and company-wide cash flow has worsened.

- Post IPO, Opera promptly directed ~$40 million of cash into businesses owned by its Chairman, including $30 million into a karaoke app, and $9.5 million into an entity used to acquire a business that Opera had already operated and funded, via a questionable transaction.

- We think Opera collapses on its own worsening financials, with that timeline accelerating significantly if Google bans its lending apps or if its Chairman/CEO continues to draw cash out of the business through questionable related-party deals.